Triumph of the HODLers

Triumph of the HODLers

Bitcoin has bubbles sometimes. So what?

Not a lot of people seem to be talking about it in the media these days, but Bitcoin has been surging in price. As I write this, it’s now up to about $48,000. That means that if you bought Bitcoin at the very tippy top of the peak in late 2017 and HODLed til now, you’re up by about 200%. If you waited til after the crash and bought on January 1, 2019, you are now up by about 1200%.

This probably teaches us some lessons about Bitcoin as an asset (or crypto as an asset class). It’s also a teachable moment about financial assets in general.

Bitcoin bubbles

Was Bitcoin “a bubble” in December 2017? I really don’t like that terminology. Finance people and pundits tend to call something “a bubble” when they think it’s overvalued — or sometimes, when they think it has no value at all and it’s going to zero. Personally, I don’t think that’s the way the term ought to be used (and I was sad when my editors used it for a column of mine after the last crash).

A bubble is when an asset rises in price and then crashes within a short space of time. It doesn’t mean the asset is valueless. U.S. stocks have had multiple bubbles over the years. Are they valueless? U.S. housing had a big bubble in the 00s, and it’s definitely not valueless.

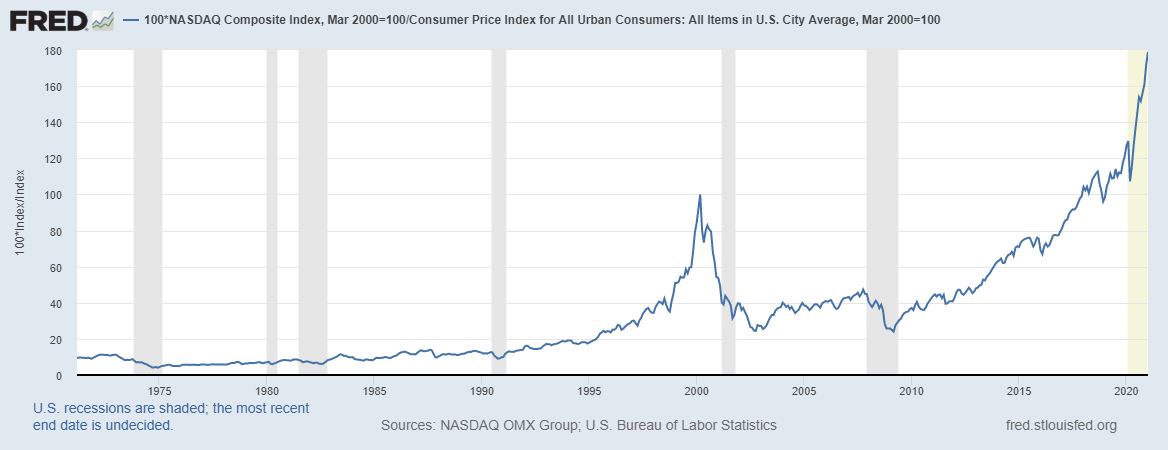

Most assets bounce back from bubbles! If you bought in at the very top of the NASDAQ bubble and held on til now, you’re up by about 80% in inflation-adjusted terms.

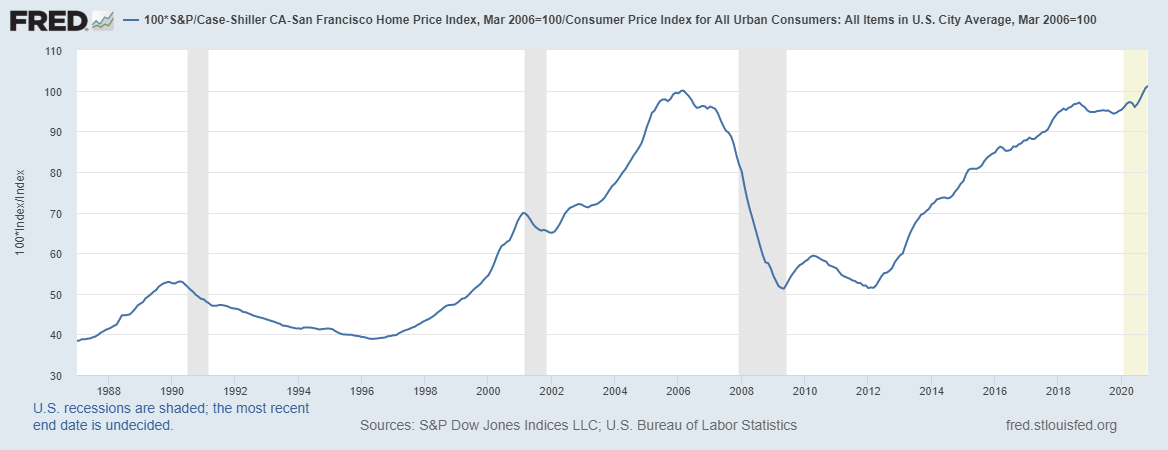

And if you bought into the U.S. housing market at the peak in 2006, congrats, you’re in the black!

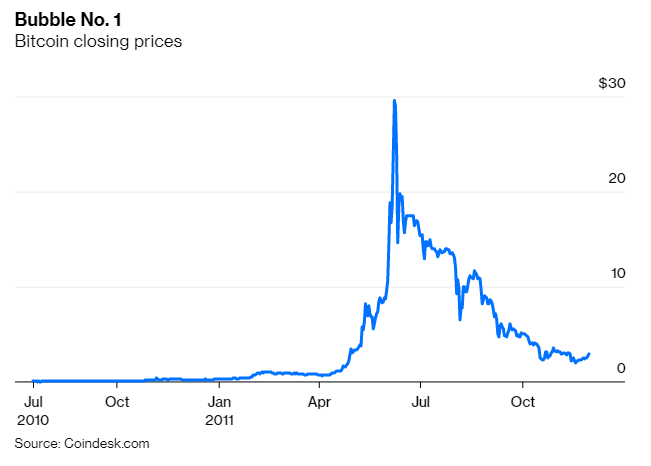

In fact, as I noted in that article three years ago, Bitcoin itself has had multiple bubbles over its lifetime. Each time it has risen to greater heights after the crash. Here was the first Bitcoin bubble, in 2011:

During that crash, Adrian Covert wrote an article in Gizmodo entitled “The Bitcoin is Dying. Whatever.” Here’s an excerpt from that article:

There’s no denying the rise of Bitcoin has been as amusing as it has been interesting. A quasi-anonymous, internet-spawned currency that shoots up to a price of $US32 is captivating. But the honeymoon is over and Bitcoin is falling. Fast…

So Bitcoin, we’ll remember the good times, like the time that one guy who got heat stroke while mining Bitcoins. Or the time there was the great heist caper that shut down trading site Mt Gox for an entire day. The lulz were abundant. But frankly, it’s time for you to go. Farewell.

Perhaps some people who had bought at the very top of the 2011 Bitcoin bubble read Covert’s article and felt a wash of despair. Well, if they held onto their Bitcoin until now, they’re up by approximately 160,000 percent. If you put $1000 into Bitcoin the day Covert’s article came out and held on, you are now a millionaire.

Now this doesn’t mean that bubbles are rational — they probably aren’t. There’s no reason that society’s best estimate of Bitcoin’s fundamental value went up by a factor of 10 and then collapsed by a factor of 5 within a few short months in 2011. Bubbles are driven by all sorts of market inefficiencies — greater-fool speculation, herd behavior, and so on. Just because an asset recovers from a bubble doesn’t mean there was a good reason to have a bubble and crash in the first place.

Nor do assets always recover from bubbles. The Nikkei is still down from its spectacular peak over 30 years ago. Gold is still down from its 2011 peak after adjusting for inflation. GameStop probably isn’t going to return to the heights of a couple weeks ago. Dutch tulips have not bounced back.

But it’s helpful to think of bubbles as just another form of asset price volatility. Stocks bounce around, and part of that is the occasional bubble. Real estate too. And crypto too.

In an efficient financial market, high volatility is correlated with high expected returns. This is one of the most basic principles of finance. Volatility is the cost that investors pay to hold an asset that is likelier to yield them bigger rewards. Risk is the pain, expected return is the gain. (Small side point here: Actually, only undiversifiable or “systematic” risk is supposed to be correlated with expected return. But since Bitcoin seems to be pretty much its own thing and is not a good proxy for stocks or bonds or gold etc., its risk doesn’t seem diversifiable.)

Now, real financial markets are not efficient. Bubbles are not efficient! Sometimes worthless, crappy assets really do pop up, get a surge of interest, then crash and go to zero. Many people over the years have argued that Bitcoin is this type of trash asset. A few people probably still do make that argument.

But let’s assume it’s not. Suppose Bitcoin’s value is slowly rising to some long-term equilibrium. The existence of semi-regular bubbles and crashes every few years will tend to slow that process, because it keeps some people scared and keeps them out of the Bitcoin market. That depresses the price today. But then as the bubbles keep happening and the skeptics realize that this is just how Bitcoin works, they eventually lose their fear and jump into the market, and Bitcoin’s price rises.

Lower initial price + same final price = higher return. Thus, in this scenario, repeated bubbles are just part of the risk-reward tradeoff. In other words, Bitcoin’s behavior so far looks exactly like that of a risky but rewarding asset that is here to stay.

So let’s think about that long-term equilibrium value. What determines Bitcoin’s true worth?

Bitcoin’s long-term fundamental value

Many Bitcoin fans believe that Bitcoin will eventually become the currency of the land — that people will eventually buy pizzas, back massages, and rent with Bitcoin instead of with U.S. dollars or other fiat currencies. If that happens, it will be money demand that will sustain the price of Bitcoin, just as money demand currently sustains the value of the dollar. I plan to write another post explaining what I think about Bitcoin’s chances of becoming the currency.

But even if Bitcoin never becomes the currency, it can still have a lot of fundamental value. It could become “digital gold”.

Gold has value for real-world uses, to be sure. But one reason gold is valuable is that some people see it as a hedge against the collapse of governments. In medieval and early modern Europe, as well as in many other premodern states, gold was used as money for cross-border payments because governments weren’t stable enough to be able to maintain stable fiat currencies. Even if we never return to that sort of anarchic world, people might want some kind of insurance against the possibility.

Gold’s current total market cap is estimated at a bit over $10.6 trillion. Bitcoin’s market cap, as of this writing, is about a tenth of that. So if Bitcoin were to become as big of a hedge against global disaster as gold is, it would probably be worth a lot more than it is now.

Another fundamental reason for Bitcoin to have long-term value is its usefulness in limited markets where normal currency can’t be used. This includes evasion of capital controls (i.e. getting your money out of China in defiance of the CCP). It includes use as a currency in places where the government has broken down, or where hyperinflation makes local fiat currency effectively useless. And yes, it includes the buying of drugs and the paying of data ransoms.

In general, all of these uses can be grouped under a single umbrella concept: System failure. The system of governments, banks, financial regulations, etc. etc. that currently runs the world is not infinitely robust. In the places and times and future conditions in which that system fails, peer-to-peer financial solutions like Bitcoin are inherently very valuable. That gives Bitcoin fundamental value.

So where does Bitcoin’s positive expected return come from? Why doesn’t it just jump up directly to this long-term value? Well, the likeliest reason is that it takes people time to get into the market. In equilibrium, lots of people will presumably want to hold Bitcoin as a hedge against system failure. But they don’t start out holding any Bitcoin. As they learn more about it, as they reassure themselves that Bitcoin bubbles don’t mean the death of Bitcoin, etc. That slow process of buy-in will produce a positive expected return, which will taper off (or even overshoot a bit) as the market reaches full buy-in.

Of course, there’s still the argument that Bitcoin will eventually die. I guess I see two ways that could happen. The first is if there’s some sort of unforeseen problem with the technology, such as if it turns out to be easier than expected to “attack” it. The second is if governments of the world unite and ban Bitcoin, and enforce their bans with harsh force. I don’t know how likely these are, but they seem to at least be theoretically possible. But governments seem unlikely to unite and stamp out Bitcoin, and the technology has held up so far, so these seem like remote possibilities.

So Bitcoin HODLing isn’t a sure bet for the long term. In fact, no financial asset on the planet is a sure bet for the long term, or ever will be. But as Bitcoin recovers from each bubble, it looks more like it’s here to stay — meaning the expected return is positive.

And Bitcoin has one more thing going for it as a financial asset — it’s really impossible to drive it out of the market. A stock can get delisted if you drive its price down far enough. A company can go bankrupt. Houses can burn down. A government can collapse. But Bitcoin, and its protocol, will always be around. If people somehow lost interest in Bitcoin and walked away and the price crashed to near 0, it would all still be there, waiting for enthusiasm to rise again and people to pick it back up. After all, that’s pretty much what just happened with Dogecoin! To kill Bitcoin, I guess you’d have to have governments basically go around and confiscate everyone’s wallets somehow. So the near un-killability of Bitcoin seems like something that adds to its fundamental value.

Which also means that efforts to denounce Bitcoin into oblivion are pretty much destined to fail.

Don’t think of Bitcoin in political terms

A lot of people denounce Bitcoin — not just saying it’s worthless, but saying it’s politically bad. Paul Krugman wrote a blog post in 2013 entitled “Bitcoin is evil”. Charles Stross wrote a post entitled “Why I want Bitcoin to die in a fire”, arguing:

BitCoin looks like it was designed as a weapon intended to damage central banking and money issuing banks, with a Libertarian political agenda in mind—to damage states ability to collect tax and monitor their citizens (sic) financial transactions.

Izabella Kaminska has likened it to QAnon (before later admitting that its fundamental value comes from a hedge against system failure, as I argued above).

The common thread in these posts and others is that Bitcoin is a political stratagem by libertarians to bring down the system, rather than simply a hedge against system failure. And this political angle often seems to influence people’s beliefs about Bitcoin’s future price path — because people think it’s evil, they expect it to fail. On Twitter, people often go further — they seem to think that if they can use social media to shame people (like Elon Musk) into refusing to buy Bitcoin, the price will crash and the whole thing will go away.

I think this is a counterproductive way to think about Bitcoin. First of all, as Barry Ritholtz teaches us, it’s bad for your finances to mix politics and investing; if you want to make money, you should assess the world as it is, not as you want it to be. Second of all, Bitcoin’s political opponents overestimate the ability of shitposting to drive the cryptocurrency into oblivion; as I mentioned before, it can always bounce back long after any temporary wave of social media shaming has passed. (Besides, shaming progressives into avoiding cryptocurrency will just mean they’re the last to get into the market, thus handing their money to libertarian early-adopters. Seems a bit self-defeating if you ask me.)

But I think the bigger point here is that the political view of Bitcoin as an anti-government weapon is just wrong. Just as the existence of gold doesn’t bring down the system, the existence of crypto won’t either. Countries and governments and corporations already have plenty of incentive not to let the system collapse; the fear of being supplanted by cryptocurrency isn’t going to make them work any harder, since they’re already working as hard as they can. As for the idea that Bitcoin could pressure central banks into lowering inflation, or replace fiat currency as the medium of exchange, that will be a topic of another post. And of course there are policy challenges associated with crypto, such as electricity usage, but that’s not a reason to think of it in politicized terms.

Anyway, the upshot of this post is that it looks like Bitcoin, and crypto in general, is here to stay — another asset class in our galaxy of asset classes. Next time there’s a Bitcoin crash — and there will be a next time — don’t panic and don’t pop the champagne. Just sit back, sip a glass of Kikusui Junmai Ginjo, and remember that financial assets go up and financial assets go down.

The thing I find most interesting about cryptocurrency is something Bitcoin doesn't support: zero-knowledge proofs. Cryptographers have come up with very elaborate mathematical schemes by which it's possible to prove to someone that a fact is true and that you know it, without revealing to them what that fact is.

Right now the main use of this is in cryptocurrencies where nobody knows where transactions come from or where they go, yet they can still be certain that all the transactions add up correctly. (I'm deliberately not mentioning the names of these because I'm not a cryptocurrency promoter, but you can look them up if you care.)

But from my limited knowledge, the zero-knowledge proof technology is pretty general, and when you think about mixing it with smart contracts, things could get pretty futuristic. Like imagine a loan, where neither party has any way of knowing who the other is, but the creditor still knows with certainty that they are the most senior creditor.

Of course the problem remains that all this is internal to the blockchain, and the real-world legal system might happily just reach in and screw it all up.

You say: "Of course, there’s still the argument that Bitcoin will eventually die. I guess I see two ways that could happen. "

Isn't there a third problem? Proliferation of alternative cryptocurrencies is effectively a glut of supply in 'systemic risk hedging assets', no? A technically superior altcoin (say, one that requires less energy expenditure) could greatly dilute the value of any other coin serving the same purpose.