Larry Summers' misplaced stimulus anxiety

Larry Summers' misplaced stimulus anxiety

Biden's relief package is big, but it's not TOO big

In late 2008, veteran economic policy adviser Larry Summers sent a 57-page memo to President-elect Barack Obama, in which — among other things — he urged him to limit the size of the stimulus that Obama was preparing in order to combat the Great Recession. Now, in a Washington Post op-ed, Summers admits the 2009 stimulus was too small, but argues that Biden’s new $1.9 trillion relief package is too large:

I agree with the general consensus of progressive economists that it would have been much better if the Obama administration had been able to legislate a much larger fiscal stimulus in early 2009, in response to the Great Recession. Yet…[T]he 2009 stimulus measures provided…$30 billion to $40 billion a month during 2009 — an amount equal to about half the output shortfall. In contrast…[Biden’s] proposed stimulus will total in the neighborhood of $150 billion a month…at least three times the size of the output shortfall…

[T]here is a chance [this] will set off inflationary pressures of a kind we have not seen in a generation, with consequences for the value of the dollar and financial stability…

Second…the U.S. economy [faces] fundamental problems of economic injustice, slow growth and inadequate public investment in everything from infrastructure to preschool education to renewable energy…[T]he stimulus proposal [contains] essentially no increase in public investment to address these challenges. After resolving the coronavirus crisis, how will political and economic space be found for the public investments that should be the nation’s highest priority?

Summers has two basic concerns: 1) inflation, and 2) deficits that will crowd out investment bills. I think he’s right to be concerned about both things, but he’s wrong in thinking that limiting the size of the package will help lessen either challenge.

Inflation

In the past, people talked as if the constraint on government was interest rates — if the government borrowed too much, the “bond vigilantes” would stop buying Treasuries and interest rates would go up, hurting the economy and limiting future borrowing. But after the Great Recession, and especially now in the days of COVID-19, it has become clear that the Fed will do what it takes to keep interest rates low. That’s why people now talk about inflation as the main constraint on government borrowing.

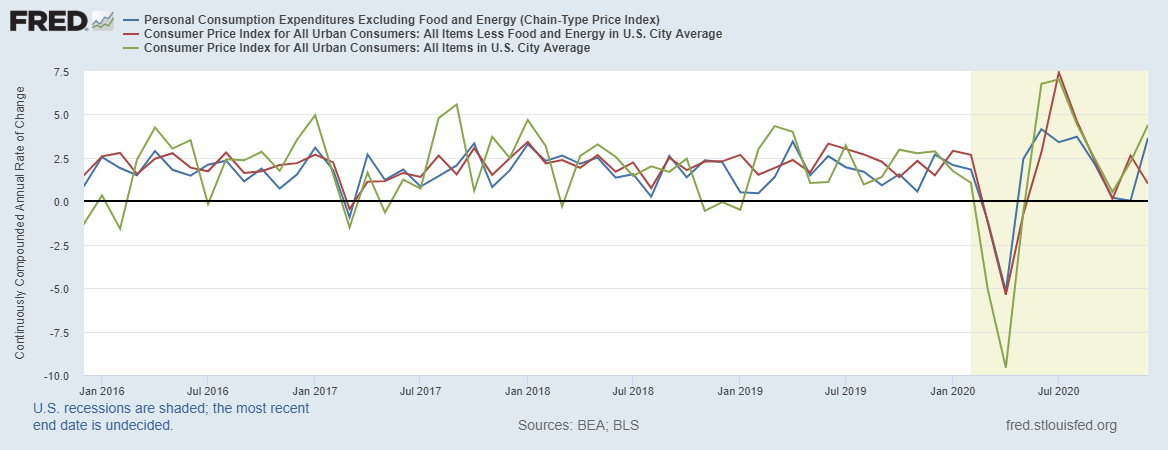

Of course, there is very little inflation in the economy right now, and hasn’t been for a long time. Here are three measures of inflation: CPI, core CPI, and core PCE (“core” meaning “not including food and energy”).

(Side note: If you think these government numbers are hiding significant inflation, you are almost certainly wrong. If you think rising asset prices are a form of inflation, you are definitely wrong. So don’t gimme any o’ that.)

So, this graph shows us a couple of things. First of all, inflation has bumped around right around the Fed’s 2% target for years. Second, the COVID-19 pandemic has seen some big zigs and zags, which may be due to the extreme weirdness of this recession, or to the difficulty of getting good data during the pandemic, or both. But so far the zigs and zags have cancelled out and we’re still right around the 2% target for 2020. Keep in mind that this is in spite of the $2.2 trillion CARES Act, which is actually bigger than what Biden is asking for now.

OK, but past performance is no guarantee of future results. We all know that. Might another $1.9 trillion (on top of December’s $900 billion) be the bale of straw that breaks the camel’s back and sends us spiraling into hyperinflation?

We can’t say for sure that it won’t. But there are two reasons not to worry too much. First, this spending is temporary stuff. People who worry about deficits causing hyperinflation typically worry that the public will decide that the central bank’s commitment to financing government deficits is a long-term, open-ended thing. But if a burst of government spending comes with an expiration date, then so does the amount of money that the Fed will have to create in order to fund it. And as soon as COVID-19 is not a big deal anymore, relief bills will stop. In fact, I don’t want to jinx it, but given the rate of vaccination this is probably the last major COVID relief bill.

Second, if inflation does materialize, there will probably be time to turn the ship around. There aren’t many studies of modern hyperinflations, but what studies there are suggest that inflation doesn’t just jump to infinity overnight; instead, there’s a sort of a prodrome period where inflation starts to go somewhat higher for a few years. Given that the U.S. has a strong, independent central bank full of people who worry about inflation, there will probably be time to turn the ship around. If inflation rises to 10% or even 6%, the Fed can start urging Congress to pump the breaks, and throttle back its suppression of interest rates.

Given all this, it seems highly unlikely that scaling the relief package back from $1.9 trillion to $1 trillion or whatever is going to make the difference in whether we experience hyperinflation, a dollar crash, etc.

(By the way, I see Jordan Weissman of Slate has just published a deeper dive into the question of whether we should worry about the inflationary effects of Biden’s relief package. Check it out.)

Investment

Summers is very right to be worried about public investment. We really need a lot of it! Where I think he goes wrong is in believing that the added debt from a larger stimulus package will be decisive in preventing investment.

If we enact Biden’s whole $1.9 trillion package, that will be a total of about $5 trillion in COVID relief spending. If we cut Biden’s proposal back significantly — say, to just $1 trillion — it will be $4 trillion total.

Ask yourself this: Do you really think the GOP, or moderate Dems like Joe Manchin, are going to be substantially less worried about the debt if we only add $4 trillion than if we add $5 trillion? Do you think that $1 trillion is really going to make the difference in whether or not they allow a big investment bill as a follow-up?

I highly, highly doubt it.

Second, if deficit hawks were thinking rationally about government finances, they wouldn’t mind the additional debt from a big green energy investment initiative. As I wrote in a recent Bloomberg post, debt-fueled green energy investment will earn a positive return on investment for the economy as a whole. Also, like COVID relief, green investment is temporary spending! If you’re worried about debt for rational reasons, there’s no reason to worry about doing a big debt-financed investment package on top of a big debt-financed COVID relief package.

But most deficit hawks are not worried for rational reasons. Moderates are worried for instinctive reasons — the debt just sorta seems Really Big. But like I said, cutting Biden’s relief package in half wouldn’t really change that instinctive perception.

As for Republicans, they’re “worried” for political reasons. They are quick enough to support deficits when the President is a Republican. Then, like clockwork, they flip to being deficit hawks when a Democrat is elected. Cutting Biden’s relief package in half wouldn’t alter this behavior one bit. Instead of yelling “OMG, look at this $2 trillion in deficit spending!”, they’d say “OMG, look at this $1 trillion in deficit spending!” And how many voters will care about that difference? Precious few.

In fact, Republicans are probably going to do the same thing with any big investment package that Biden proposes, no matter what happens with COVID relief.

A better solution to the problem is to put lots more investment in the relief bill. There’s no reason we can’t do this — in fact, we already did it in the December COVID bill! Yes, pandemic relief comes first, but we can start scheduling investment projects for a year or two years from now.

Anyway, it just seems unlikely that we can increase the chances of getting a big investment package passed later by slashing the size of COVID relief today. Instead, this seems like just another example of the kind of self-defeating preemptive concession-making that hobbled Obama’s first term. If Summers is really and truly worried about the size of Biden’s package, he can sit back and reassure himself that the Republicans and moderates will probably be able to shrink it substantially before it passes. I doubt we’re actually going to get $1.9 trillion. But we might as well ask.

Larry Summers needs to be more concerned about the details that keep coming out about how close he was to Jeffrey Epstein........

At this point, Summers just goes against what everyone else is saying for the sake of it. We have an abysmal economy that has gotten exponentially worse for working-class families since the 2008 recession. Although Summers is a respected figure in economics (that is still somewhat "liberal"), he hasn't offered any serious solutions to pressing issues rather than just try to poke holes and raise doubt about new ideas from other more progressive economists (Saez, Zucman, etc).

Great article by the way! So glad I found this blog and I subscribed to Bloomberg to read your articles!