Crypto and the global financial system

Crypto and the global financial system

Are we headed for financial anarchy?

The global financial system is something that humanity controls but doesn’t really understand. There are plenty of theories out there as to how the system works, but they’re all pretty abstract. And yet we have to have a global financial system, because without one, it’s very difficult to have international trade, international borrowing and lending, bailouts for countries in crisis, and a bunch of other stuff that’s necessary for the economy to function. So we set up rules and institutions without really knowing whether they’re optimal or when they’ll break down. It’s not surprising, therefore, that the system experiences crises and major disruptions every once in a while.

Recently, there’s been some talk of cryptocurrency disrupting the global financial system. For example, Balaji Srinivasan and Parag Khanna recently wrote an op-ed that got a lot of attention, in which they assert that cryptocurrency, along with other internet technologies, will disrupt the nation-state system itself. Here’s what they wrote about the financial aspect:

Already, national currencies compete with cryptocurrencies because individuals and institutions hold digital wallets filled with various assets that can be traded against one another…

We are about to enter an age of global monetary competition, where national currencies must earn their place in someone’s wallet portfolio every hour of every day, even among citizens of their own countries. The digital version of the Japanese yen will be plunged into head-to-head global competition with the Swiss franc, the Brazilian real, and any other asset with an open capital account, including Bitcoin. Everyone becomes a foreign-exchange trader, all the time, and only the best national currencies—or cryptocurrencies—are ever held by anyone.

Rather than the current environment of unchecked inflation and competitive devaluation, the defi [decentralized finance] matrix imposes a new kind of discipline on national currencies, as billions of people make individual choices regarding which currencies to hold—or not hold.

Srinivasan and Khanna’s vision of the future is very different and more sophisticated than the traditional “Bitcoin maximalist” view. Briefly, the Bitcoin maximalist view is that because Bitcoin is artificially scarce and thus tends to appreciate rather than depreciate, it represents better money than inflationary fiat currencies, therefore people will switch from fiat to Bitcoin. This is wrong because what people want out of their money is not long-term appreciation but rather short-term stability; that’s why no one uses gold, Apple stock, or Bitcoin to buy a loaf of bread or a gallon of gas.

But crypto isn’t just Bitcoin anymore. Indeed, Bitcoin itself may eventually become a sort of beloved obsolete appendage of the crypto world, as more sophisticated systems (Ether, Solana, etc.) exploit more of the technological potential of blockchains. Srinivasan and Khanna actually envision government-supported cryptocurrencies competing with each other. And out there in the market, stablecoins are blurring the line between fiat and crypto.

Given this technological ferment, it’s worth asking how crypto might change the global financial system. Which is a difficult thing to ask, because not only do we not know what crypto is doing right now, let alone what it’ll be doing in 20 years, there’s plenty we don’t even know how the global financial system works in the first place!

But we can certainly start…um…speculating.

The status quo: Bretton Woods II

First, let’s talk a little bit about how the global financial system currently works (we don’t know everything, but we know a few details). Usually there’s a “reserve currency” — one currency that the central banks of most or all of the major economies keep a lot of in reserve. They do this for two reasons: First, because it makes international transactions easy; globally traded commodities like oil are typically priced in dollars. Second, if a country has a financial crisis, it can sell those reserves to stop its currency from crashing, so it can keep importing necessities. The reserve currency thus functions as both a facilitator of global commerce and as a safe haven.

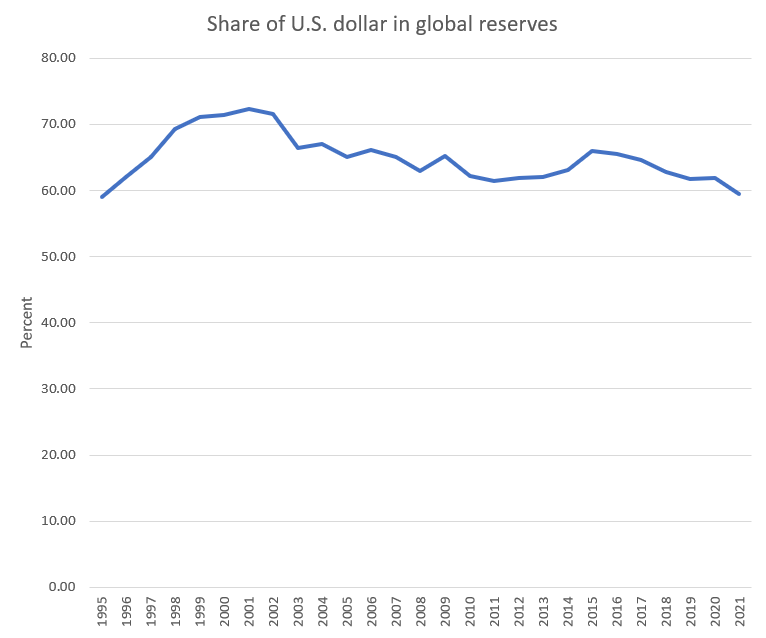

In the 19th and early 20th centuries, it was the British pound. Right now, it’s the U.S. dollar. This system is sometimes called “Bretton Woods 2”, which is a reference to the postwar Bretton Woods system in which major economies agreed to use dollars as the reserve currency. Bretton Woods was scrapped in 1973, and the dollar share of global currency reserves plummeted from around 84% to around 46%. But the dollar made a comeback in the late 90s and early 00s, rising back above 70%. Hence, “Bretton Woods 2”.

Since the mid-00s, however, the Bretton Woods 2 system has come under increasing pressure. The main cause is the rise of China. As China’s economy grows — it’s now either bigger than the U.S. or almost as big, depending on what measure you use — its potential to either suck in capital from overseas or send capital overseas becomes larger. For example, China exported a ton of capital in the 00s when its central bank bought a ton of U.S. bonds (in order to keep its currency cheap and pump up exports). It also exported a ton of capital in 2015-16, when a bunch of investors moved their money out of the country following a stock market crash.

Those capital flows have to be absorbed by the U.S. economy, which no longer dwarfs China’s the way it used to. And that can be destabilizing. Chinese capital inflows during the 00s are sometimes blamed for the U.S. housing bubble, for example. The dollar’s reserve currency status also causes the U.S. to run persistent trade deficits — everyone wants to hold dollars, so demand for dollars goes up, dollars get more expensive, and U.S.-made goods thus become unaffordable in world markets.

The less dominant the U.S. economy is, the less the dollar can function as a stable anchor for the global financial system. It was still intact in 2008-10, when a global financial crisis sent capital flooding to the safe haven of U.S. government bonds. But in recent years, people have begun to question whether Bretton Woods 2 is finally on the way out. The share of U.S. dollars in global reserves has been falling for years, and this fall has accelerated since the start of the pandemic.

But what can replace Bretton Woods 2? The obvious answer would be for the Chinese yuan to either take over as reserve currency the way the dollar took over from the pound, or to share duties with the dollar and euro. But China seems to have zero intent of ever relaxing its capital controls and allowing the world to buy as much yuan as they like. That means the yuan can’t fill the dollar’s shoes.

So this might someday open the door to cryptocurrencies acting as reserve currencies in some respect. Probably not this year, maybe not this decade, but perhaps in 20 years? Even more radically, crypto might do away with the need for a reserve currency at all.

Stablecoins, the dollar, and the new reserve currency

One big innovation in crypto is the stablecoin. The most famous of these is Tether, but USD Coin is also gaining popularity, and there are a bunch of others as well. Stablecoins are cryptocurrencies whose value is pegged to the value of a fiat currency (actually there are some different kinds, but Tether and USD Coin are this kind). That means that 1 Tether or 1 USD Coin is always supposed to be worth US$1.

The initial idea of stablecoins was to be a sort of compromise between Bitcoin and fiat money. The reason people don’t use Bitcoin to buy pizza is that its value jumps around a lot — you don’t know how much you’re actually spending on pizza. Much better to spend a dollar instead — because dollar inflation is usually low and stable, you know exactly how much value you’re giving up in exchange for your pizza. But if a Tether (referred to as 1 USDT) or 1 USD Coin (1 USDC) is worth $1, you can theoretically use USDT or USDC to buy your pizza and it works just as well as $1.

So far, people don’t use stablecoins to buy pizza. But they do use stablecoins a whole lot in crypto financial transactions, to the point where some claim that Tether underpins the entire emerging crypto financial system. In other words, if cryptocurrencies are like countries, then Tether is acting like the reserve currency.

Of course, Tether can’t just mandate that 1 USDT = $1. It has to support that valuation in a market. So Tether maintains dollar reserves, so that if someone tries to buy or sell USDT’s value away from the pegged value of $1, the Tether company will either create new Tethers or use its dollar assets to restore USDT to a value of $1. This is similar to the way foreign countries peg their currencies against the dollar.

If Tether has US$1 in reserves for every Tether it issues — as the company claims it does — it can always maintain the peg. But there has been a lot of scandal surrounding Tether, because the company is probably lying about how much dollar assets it has. Most observers believe it has a lot less than US$1 per USDT, and the company has been fined by the U.S. government for not having as much reserves as it claims.

This makes Tether look somewhat like the return of a vanished 19th-century financial institution: The fractional-reserve free bank. Back in the 19th century, banks in the U.S. issued their own dollars — it would be like if we had Chase dollars and Citibank dollars and Wells Fargo dollars, instead of just the good old green government-printed dollars that we use today. They had to keep reserves (of gold and/or silver), but these reserves didn’t have to equal the amount of currency issued — only a fraction of it. Fractional reserve banking allows banks to make profit, since they can lend out a lot more than they take in deposits, but it also makes them vulnerable to bank runs; if everyone asks for their money back at once, the bank can’t make payments, and either gets bailed out by the government or goes out of business.

Similarly, Tether, if it is indeed creating a lot more USDT than it has dollars in reserve, is engaging in fractional-reserve banking and creating its own dollars. Of course unlike the free banks of the 19th century, Tether would be doing this illegally (which is why it got fined).

But so what? Even if it’s being fraudulent, that doesn’t mean Tether is worthless or that it’s not providing economic value. That just makes it a poorly-regulated gray-market fractional-reserve bank. As Cem Dilmegani explains, there is probably not going to be a run on Tether anytime soon — most of the USDT is held by a few big accounts that are unlikely to demand their dollars back from the company. So if there’s not a run, everything is fine. And if there is a run, well, the crypto people knew the risks.

As for USD Coin, Tether’s main competitor, it claims to be fully backed by “fully reserved assets”. These include things like Treasuries. Assuming the company is telling the truth (which it probably is), that makes USD coin less like a fractional-reserve bank and more like a money market fund. A money market fund invests in highly liquid low-risk assets like Treasuries, and issues its own shares, which are then traded as if they are practically as good as dollars. They only run into trouble in extreme situations, like in 2008 when it turned out that many money market funds were holding assets that were not nearly as low-risk as they thought.

So Tether and USD Coin aren’t replacing fiat money. Instead, they’re transposing well-known financial institutions into the cowboy world of crypto. This could ironically extend U.S. dollar hegemony, at least in the short term, because stablecoins could make it easier for gray markets to get their hands on dollar equivalents. For example, in 2019 and 2020 Tether was widely suspected of being a vehicle for capital flight from China, helping people get their money out of China and into dollars. Future stablecoins that ensured total privacy via zero-knowledge proofs might be even more effective at letting people circumvent capital controls without consequences.

But Bretton Woods 2 is still under pressure, and in the long term, creating new cryptodollars doesn’t change any of the underlying economic problems with dollar hegemony. And stablecoins could play a very interesting role in creating a new equilibrium — whether or not China ever allows yuan convertibility.

Stablecoins don’t have to be valued at $1. They could be valued at some basket of currencies — $1 + 1 euro + 5 yuan, or whatever. In other words, they’d be private versions of the IMF’s Special Drawing Rights. And if cryptocurrency becomes widely used throughout the world, those SDR-like stablecoins (SDR Coin, anyone?) might actually become the global reserve currency. That might be an arrangement well-suited to a permanently multipolar world where no single economy dominates the globe the way the U.S. once did.

Global financial anarchy?

Now we come to even more radical scenarios — the global financial anarchy envisioned by Srinivasan and Khanna. Remember, they forecast a world where everyone is able to use any currency anywhere at any time. If you’re in Chile, and you’d rather pay for your pizza with Indian rupees than with Chilean pesos, then you can just do that — assuming the pizza restaurant is OK with that.

There’s just one problem with this: Countries would completely lose control over their own monetary policies. Normally, the Banco Central de Chile can control interest rates (and affect both inflation and growth) within Chile’s borders by creating or destroying Chilean pesos and exchanging them for financial assets. But if everyone in Chile is using Indian rupees, then it’s the Bank of India that actually controls interest rates, inflation, and growth in Chile. Yes, Chileans would still have to pay their taxes in Chilean pesos, but with ubiquitous frictionless currency markets on every mobile device, this would be super easy to do, and would not be a reason to hold or use pesos most of the time.

The Chilean government wouldn’t want this, of course, since it wants to be able to control its own monetary policy. And it would be fairly easy to stop. Yes, trying to ban cryptocurrencies completely would would inaugurate the great dystopian sci-fi war between nations and cryptocurrencies that some people have been anticipating for a while; something like this is currently playing out in China, where the government is attempting to hunt down Bitcoin miners.

But in order to prevent crypto-rupees from becoming the currency of Chile, all the Chilean government has to do is to raise the risk of using them. Remember, people use money because it’s reliable and low-risk. If buying a pizza with rupees means I might get a pizza or I might get a jail sentence, I’ll definitely use pesos. Drug users and money launderers and ransomware pirates will still use crypto in defiance (defi-ance?) of the laws, and chaotic, collapsing states like Venezuela will use crypto-dollars instead of their failing local currencies, but most people in most countries will use what the law tells them to use.

Similarly, finance will remain nationalized if governments decree it. Decentralized stablecoins might act like organization-less banks, lending Rupee Coin to Chilean businesspeople through defi algorithms, but only if the Chilean government allows it. If taking out a loan in Rupee Coin entails the risk of jail, people will usually opt for less risky means of finance, even if it means paying a slightly higher interest rate.

In other words, while stablecoins and other new crypto products might transform the international financial system, I do not see much possibility of the global financial free-for-all that Srinivasan and Khanna envision. Governments want to maintain a monopoly on their monetary policy, and as long as they retain their monopoly on the use of force, they will have the tools to do so. At most, I see crypto eating away at the edges of government control, increasing the size and reach of black markets and gray markets, and allowing companies in developing countries to borrow in foreign currencies more easily. The latter may create more emerging market crises (since borrowing heavily in foreign currencies puts countries at risk from currency depreciation). But ultimately that will be a modest change.

This thought exercise should be reassuring. When it comes to the global financial system, crypto represents an opportunity rather than a threat. It could help rebalance the international reserve currency away from its unhealthy dependence on the U.S. dollar. But it won’t result in global financial anarchy, the collapse of independent monetary policy, or the end of nation-states. That should probably make you feel a bit better about it.

* Note: It is strange to refer to my old friend Balaji by his last name, when we have always simply referred to him as “Balaji”. But I don’t know Parag Khanna very well, so for the sake of symmetry and formality I was forced to use their last names…

Awesome read. Loved this. My thoughts: If decentralized countries, with diasporic peoples, offer enough to centralized countries where some citizens of their nation reside, decentralized will be able to leverage financial systems in their favor. If not, it would be X centralized govt interests vs. decentralized govt interest AND corp interests that prefer the decentralized finance system. That changes the game theory of whether a centralized country outlawed or mandates payments their own reserve currency. So I think we will get closer to this anarchy scenario than you think, and sooner.

Nice post. I wonder: what about capital markets?

The 1998 Asian crises were partly about a whole lot of dollars flowing out even faster than they flowed in. Should we expect some country next decade to hit a "crypto financial crisis," where they attract a lot of crypto investment and then face sudden capital flight?

Maybe a crypto hot-money crisis world work the same as in regular currencies. But capital controls, for example, could be much harder to impose in an emergency on crypto-denominated investments: they don't need banks to move money.

Likewise, a crypto-normalized world should make it much easier for Iran or China or North Korea to get around sanctions. Unless the OECD start regulating crypto transactions, of course, but you could imagine a decade of gap between the problem and the regulations to fix it.

Are there other differences we could expect?