Why has climate economics failed us?

Why has climate economics failed us?

Economists could have helped in the fight against climate change. So far, they haven't.

Ezra Klein has an excellent post at the New York Times on the politics of Bidenomics. This part really caught my eye:

Biden has less trust in economists, and so does everyone else…

Multiple economists, both inside and outside the Biden administration, told me that this is an administration in which economists and financiers are simply far less influential than they were in past administrations…

The backdrop for this administration is the failures of the past generation of economic advice. Fifteen years of financial crises, yawning inequality and repeated debt panics that never showed up in interest rates have taken the shine off economic expertise. But the core of this story is climate…

Economists have their ideas for solving climate change — a hefty carbon tax chief among them — but Biden and his team see this as fundamentally a political problem. They view the idea that a carbon tax is the essential answer to the problem of climate change as being so divorced from political reality as to be actively dangerous.

It’s interesting to see which branches of econ are gaining clout in Democratic administrations and which are losing clout. On one hand, Biden’s cash-based welfare programs and big R&D spending come firmly out of economics research. On the other hand, he seems to be paying much less attention to austerity-minded macroeconomists.

But as Ezra points out, it’s climate where economists are being utterly ignored, in favor of technologists and activists. And rightly so. I hate to say this, but climate economics has almost completely failed to be useful to the national policy discourse. This isn’t a minor slip-up, either; climate change is one of the most important economic policy issues for the future of the country and the world, and the econ profession has just totally dropped the ball.

I wrote a Bloomberg article about this back in 2016, but the situation hasn’t noticeably improved. I can see at least four major ways climate economics has failed. These are:

Simply not publishing enough research

Putting out models that are frankly just bad

Ignoring tail risks

Obsessively focusing on carbon taxes

Criticizing academic economists is tough. They tend to instantly circle the wagons and scoff dismissively at any external critics. And why shouldn’t they? With their tenure and high salaries, they don’t exactly have much of a financial or professional reason to care if some blogger chides them, or even if the President refuses to heed their advice. But there are lots of good people within the profession who have strong consciences, and who don’t like the idea of economics falling into disrepute and losing influence. So I hope criticisms like this reach the ears of people who quietly realize the need to change course.

Ignoring climate

One big problem with climate economics is that there just isn’t enough of it. Climate change is going to affect every facet of our economy. Quantitatively, it’s vastly more important than any optimal tax calculation or detail of occupational licensing; it’s arguably even more important than the business cycle itself. But the number of papers at top journals dedicated to climate economics is miniscule. In a scathing 2019 article entitled “Why are economists letting the world down on climate change?”, economists Andrew Oswald and Nicholas Stern write:

We are sorry to say that we think academic economists are letting down the world. Economics has contributed disturbingly little to discussions about climate change. As one example, the Quarterly Journal of Economics, which is currently the most-cited journal in the field of economics, has never published an article on climate change…

We suspect that modern economics is stuck in a kind of Nash equilibrium. Academic economists are obsessed with publishing per se and with pleasing potential referees. The reason there are few economists who write climate change articles, we think, is because other economists do not write climate change articles.

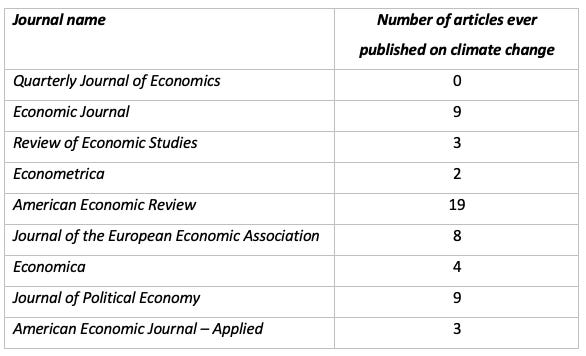

They include the following table, which shows just how few climate papers the top econ journals have ever published as of 2019:

The total is 57, out of a total of approximately 77,000 total articles. So about 0.074%.

As Oswald and Stern point out, this is really surprising, since climate change A) is caused by economic activity, B) has huge economic effects, and C) will take smart economic policy to get out of.

In fact, though, I think the situation is even worse than their article depicts. Because a fair amount of the climate economics research that does get done is badly flawed.

Bad research

The most egregious strain of climate economics research is the stuff that concludes that climate change is not a problem at all. The chief offender here I know of here is Richard Tol, a professor at the University of Sussex. Tol wrote a famous paper in 2009 in which he argued that global warming would cause economic gains for people living in temperate zones, and that these gains would outweigh the losses to people living in the tropics. His reasoning? Warmer temperatures mean you don’t have to use the heater as much, warm temperatures are better for health, and more CO2 in the atmosphere makes crops grow faster.

This is obviously ridiculous, for any number of reasons that a few seconds of thought by anyone even remotely acquainted with the climate change issue can easily point out. First of all, climate change doesn’t just warm everything up gently and evenly; it causes erratic weather, which can include very cold weather (this was widely understood well before Tol wrote his paper). Second, an overwhelming amount of research shows that climate change is bad for agricultural productivity, through a vast array of mechanisms; Tol simply cherry-picked one random paper that claims CO2 makes plants grow faster.

Third, there are a ton of effects of climate change that Tol waves away, saying they “seem likely to be small”. The word “wildfires” does not appear in his article. Tol recognizes this problem, writing that “negative surprises should be more likely than positive surprises” and “it is relatively easy to imagine a disaster scenario for climate change,” and then basically ignores that crucial point.

But on top of all this, Tol’s calculations were complete crap. In 2014 he had to publish a correction when it turned out he had omitted some minus signs, causing him to log costs of climate change as benefits (ooops!!). He also made a coding error that dropped some data. Tol blamed “gremlins” for the errors. Andrew Gelman and company found a whole raft of additional problems with Tol’s data, analysis, and model. In 2015, the journal issued a second round of corrections.

This was obviously an incredibly poor showing. But Tol’s shoddy analysis made its way into the public policy conversation. In 2009 he published an op-ed entitled “Why worry about climate change?”. Senate Republicans put him on their list of expert climate change skeptics. As recently as 2013 — before all the gremlins were discovered — Tol’s bad research was being used by conservative op-ed writers to argue that climate change is good for the world.

So is Tol a lone outlier here? It’s hard to find research as bad as that 2009 paper, but many of the same basic errors crop up in other climate economics research. For example, in 2011, Michael Greenstone and Olivier Deschenes published a paper about climate change and mortality (I studied an earlier version of this paper in a grad school class). Their approach is to measure the effect of temperature on mortality rates in normal times, and use that estimate to predict how a warmer world would affect mortality.

The authors make the obvious and grievous mistake of assuming that climate change affects human mortality only through the direct effects of air temperature — heatstroke, heart attack, freezing, and so on. The word “storm” does not appear in the paper. The word “fire” does not appear in the paper. The word “flood” does not appear in the paper. The authors do mention that climate change might increase disease vectors, but wave this away. Near the end of the paper they write that “it is possible that the incidence of extreme events would increase, and these could affect human health…This study is not equipped to shed light on these issues.”

You don’t say.

The big conceptual mistake here is to assume that whatever economists can easily measure is the sum total of what’s important for the world — that events for which a reliable cost or benefit cannot be easily guessed should simply be ignored in cost-benefit calculations. That is bad science and bad policy advice.

Greenstone and Deschenes also published a paper in the prestigious American Economic Review in 2007 in which they conclude that global warming will increase crop yields. This conclusion is very different from what most researchers find, including other climate economists. Economists Anthony Fisher, Michael Hanemann, and Michael James Roberts published a comment in 2012. They write:

In a series of studies employing a variety of approaches, we have found that the potential impact of climate change on US agriculture is likely negative. Deschênes and Greenstone (2007) report dramatically different results based on regressions of agricultural profits and yields on weather variables. The divergence is explained by (1) missing and incorrect weather and climate data in their study; (2) their use of older climate change projections rather than the more recent and less optimistic projections from the Fourth Assessment Report; and (3) difficulties in their profit measure due to the confounding effects of storage.

Michael Greenstone, a professor at the University of Chicago, is a very important and influential climate economist! He helped lead the Obama administration team tasked with calculating a numerical value for the “social cost of carbon”. When important, leading researchers put out papers ignoring the biggest dangers from climate change and producing highly unusual results with potential data errors, we should be worried.

Why is this bad climate economics research getting published? Many people will be quick to allege that it’s politics — conservative economists who believe that anxiety over climate change is an excuse to destroy capitalism, and who are thus biased towards doing research that minimizes the potential harm of climate change. I don’t know how much of that is going on, but I think there are also other potential reasons.

One is the streetlight effect — economists are very focused on what they can measure, and tend to disregard what they can’t measure.

A second is siloing — economists are not the type to go call up climate scientists to collaborate on a paper. If you look at the references in one of Deschenes and Greenstone’s papers, you see very few citations of actual climate science papers; instead, it’s mostly just a bunch of econ papers. You’d think that collaboration with the scientists who study the actual physical process of climate change and its associated effects on weather, crops, and so on would seem to be crucial for assessing the economic impact of climate change…right?

In any case, my suspicion is that this sort of research contributes to the growing conviction that climate economists are not experts to be relied upon.

DICE models

If there is one climate economist who is respected above all others, it’s William Nordhaus of Yale, who won the Econ Nobel in 2018 “for integrating climate change into long-run macroeconomic analysis.” The prize specifically cited Nordhaus’ creation of an “integrated assessment model” for analyzing the costs of climate change. The most famous of these is the DICE Model, used by the Environmental Protection Agency.

But the DICE Model, or at least the version we’ve been using for years, is obviously bananas. As climate writer David Roberts noted in 2018, according to the standard version of Nordhaus’ model, the economic cost of a 6°C increase in global temperatures would only be 10% of GDP. As Roberts notes, climate scientists believe that that level of temperature increase would make the Earth basically unlivable. An unlivable Earth is going to cost a lot more than 10% of GDP.

Nordhaus’ models recommend a ceiling of of 3.5°C, which is higher than what the world is on track for at the end of the century if we don’t make any further changes; in other words, a Nobel-winning climate economics model recommends that the economic cost of doing anything more than we’re already doing to stop climate change is too high.

That’s obviously bananapants, so let’s go through and discuss a couple obvious problems with the model.

One obvious problem with DICE models, or at least with the numbers Nordhaus plugged into his DICE models, is that they assume a high discount rate. The discount rate is the degree to which we don’t care about the future — the higher the discount rate, the more we disregard what happens in 20 or 50 years. DICE models get their discount rate from interest rates, which represent how much the investors who are currently alive and investing in the market care about the future. If investors’ bond purchases don’t reflect concerns about whether their great-grandchildren live in an infernal hellscape, DICE doesn’t care about it either.

It turns out that most economists think that this isn’t a good way to select discount rates. In 2016, David Roberts reported the results of a survey of economists who mostly supported using a lower discount rate than the market rate, based on ethical concerns about the future of humanity:

This is obviously the right thing to do, and economists know it, yet somehow the most popular climate model for years was one that ignored the welfare of future generations.

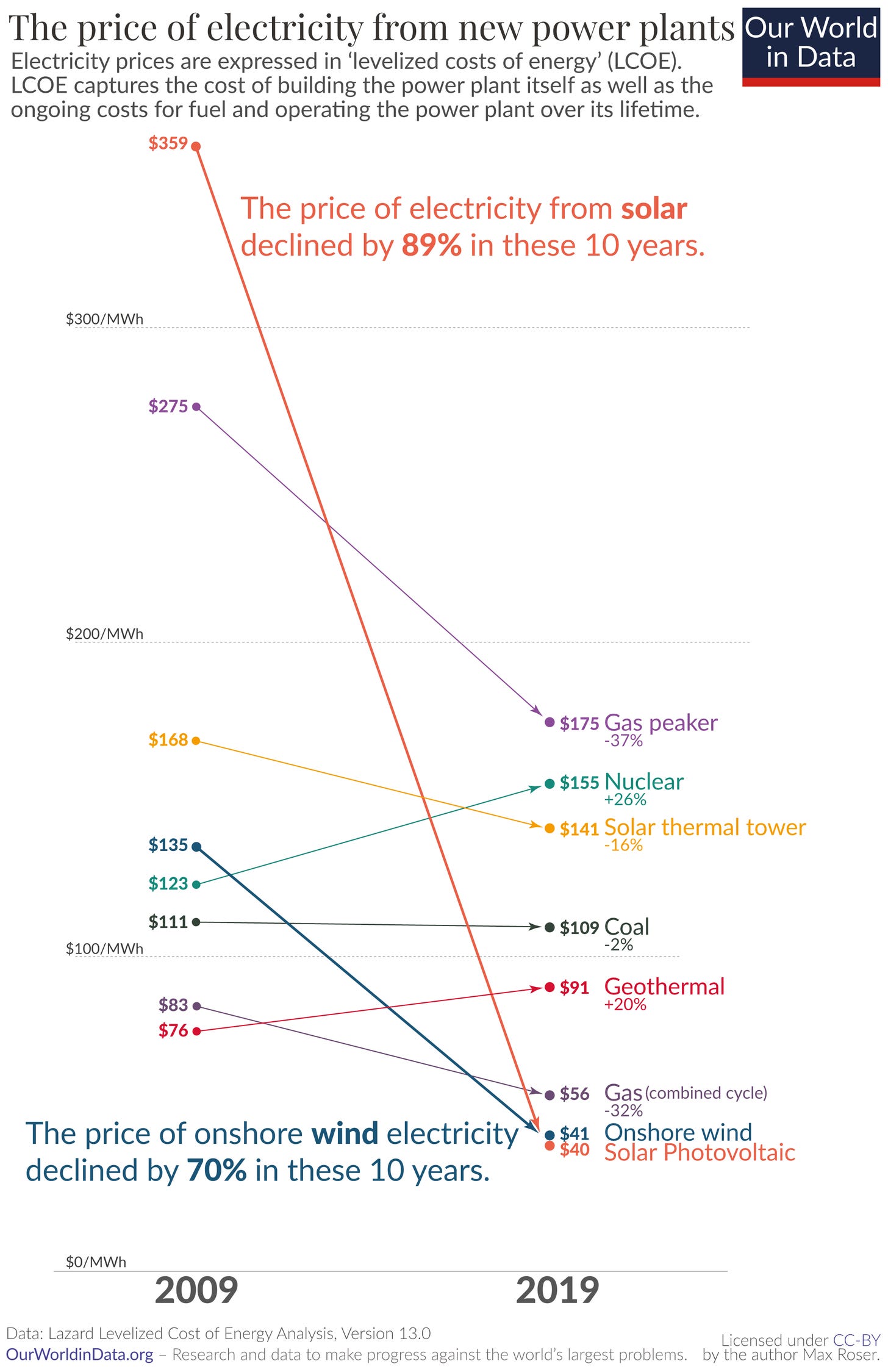

A second reason DICE models are broken is that they assume that stopping climate change will be very expensive. Nordhaus’ formulation basically ignores the fact that renewable energy technologies have been getting cheaper at a stupendous rate for decades, which reduces the cost of decarbonization. Once more I must post this graph:

In other words, DICE models basically assume that we face a grim choice between impoverishing ourselves today or forcing our descendants to endure a hellscape future — and having tricked themselves into believing this, they choose to save the economy rather than the future of humanity. But thanks to technological progress, this grim choice is no longer nearly so grim.

In addition to all of this, the DICE models probably get the climate science wrong. In 2020, a group of climate scientists writing in Nature Climate Change concluded:

Under the UN Paris Agreement, countries committed to limiting global warming to well below 2 °C and to actively pursue a 1.5 °C limit. Yet, according to the 2018 Economics Nobel laureate William Nordhaus, these targets are economically suboptimal or unattainable and the world community should aim for 3.5 °C in 2100 instead. Here, we show that the UN climate targets may be optimal even in the Dynamic Integrated Climate–Economy (DICE) integrated assessment model, when appropriately updated. Changes to DICE include more accurate calibration of the carbon cycle and energy balance model, and updated climate damage estimates.

A team of economists looked closely at the science and reached the same conclusion. Put more reasonable costs and discount rates into a DICE model, and it gives us a target closer to 2°C — exactly what climate scientists have been recommending.

But on top of all this, there’s one other huge weakness of the DICE model — it focuses on the most likely scenario, and ignores tail risks. As Richard Tol wrote, “negative surprises should be more likely than positive surprises” when it comes to climate change, and “it is relatively easy to imagine a disaster scenario for climate change.” The possibility of very bad effects of climate change that we can’t predict should make us more anxious to avoid it. Some of these are things we can imagine but which we think have only a small probability, like “tipping points” beyond which climate change becomes self-sustaining. And others are things we don’t even consider before we wake up and find them happening to us. In September 2020, Oregonians woke up and found this happening to their world:

Lots of people moved to California for the weather. If wildfires, driven by climate change, make the state unlivable, that will be an economic cost not imagined by William Nordhaus models. What other things did Nordhaus fail to imagine?

There was one famous economist who did imagine these things. Martin Weitzman wrote a paper in 2009 called “On modeling and interpreting the economics of catastrophic climate change”. The math is complex, but the upshot is simple and easy to understand: If there’s the possibility of utter catastrophe, standard cost-benefit analysis doesn’t make a whole lot of sense. Weitzman wrote:

Perhaps in the end the climate-change economist can help most by not presenting a cost-benefit estimate for what is inherently a fat-tailed situation with potentially unlimited downside exposure as if it is accurate and objective…the artificial crispness conveyed by conventional [DICE-type cost-benefit analyses] here is especially and unusually misleading compared with more ordinary non-climate-change CBA situations.

Weitzman tried to warn us. Instead, despite widespread expectations he would share the Nobel with Nordhaus, he was snubbed — one of the prize committee’s most grievous errors, in my opinion.

The carbon tax fetish

On top of all these problems with climate economics research, the main policy that climate economists recommend is utterly inadequate to the task of dealing with climate change. I’m talking about carbon taxes.

Economists LOVE carbon taxes. Voters seem not to. In 2016, economist Yoram Bauman — best known for doing inside-baseball stand-up comedy about the economics profession (a show I once participated in!) — launched a campaign to create a revenue-neutral carbon tax in the state of Washington. Despite basically every economist in the world gushing over it, it failed 59.3% to 40.7%. It met stiff opposition from the political left and didn’t get much support on the political right either. Greg Mankiw created the Pigou Club, which in his words was “an elite group of economists and pundits with the good sense to have publicly advocated…carbon taxes.” This elite group has accomplished just about as much as you might expect. A second Washington State effort, designed to be more amenable to the left, went down to defeat in 2018.

In 2019, some economists studied these failures and tried to figure out why voters, despite liking a carbon tax in polls, voted it down at the voting booth. They found that ideological opposition and pressure from special interest groups was a factor, but they also found that people were simply averse to paying higher energy prices.

This isn’t just politics; economists have forgotten basic Econ 101. Voters instinctively know what economists, for some mystifying reason, have seemed to ignore — the people who pay the costs of a carbon tax don’t reap the benefits. Carbon taxes are enacted locally, but climate change is a global phenomenon. That means that if Washington state taxes carbon, its own residents pay, but most of the benefit is reaped by people in other countries and other states. Thus, jurisdictions that choose not to enact carbon taxes can simply hope that someone else shoulders the cost of combating climate change. So no one ends up paying the cost.

That’s called the free rider problem, and it’s one of the most basic forms of market failure. When economists urge nations and states to tax carbon, they are hoping that altruism will overcome the free rider problem. It generally does not. Only a few countries around the world have put a price on carbon.

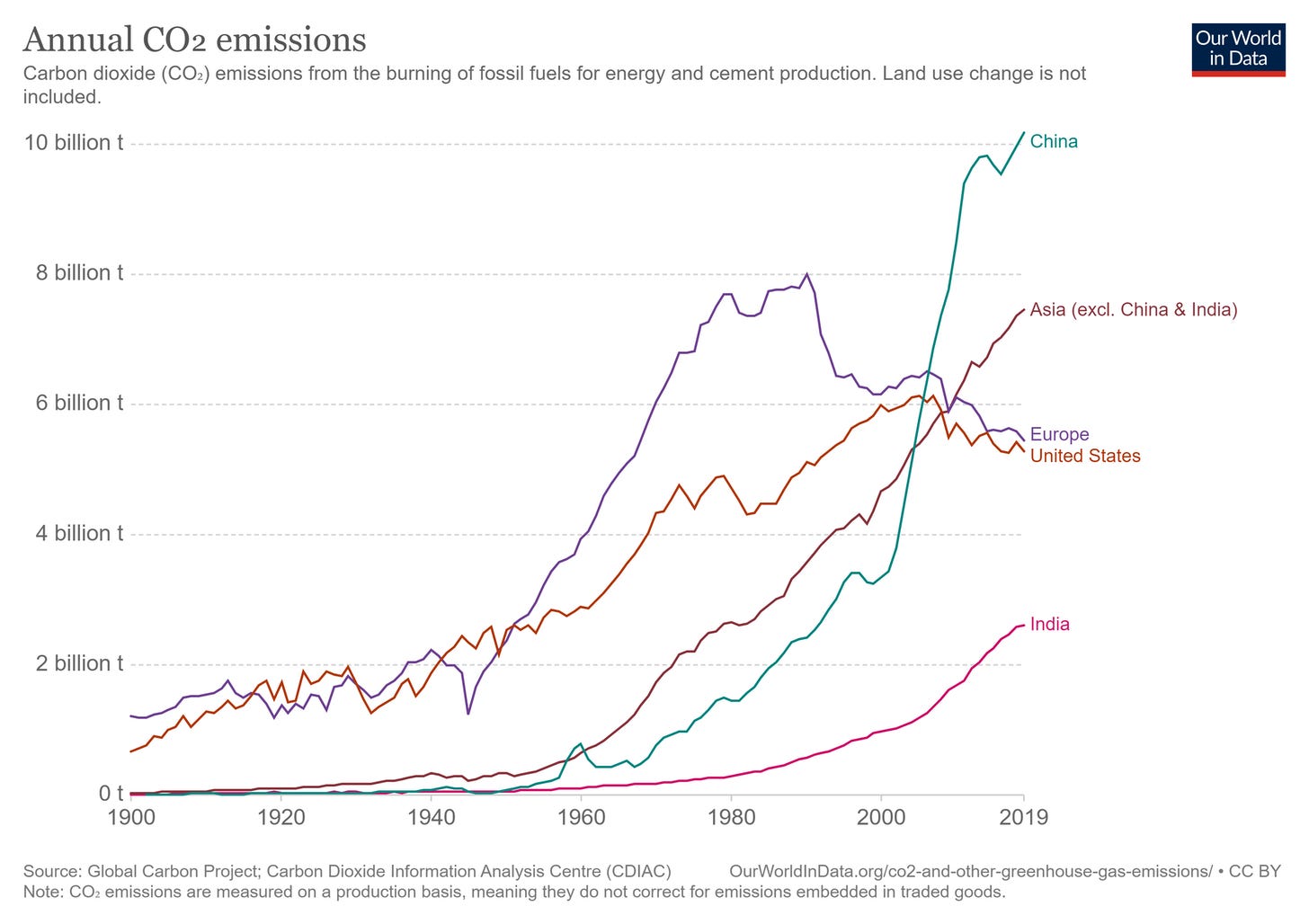

The free-rider problem is especially acute for rapidly growing poor countries. These countries now produce the lion’s share of the world’s carbon emissions, and that share is only going to grow:

If warming is to be held to 2°C, it is these countries that must do the lion’s share of the decarbonization. If doing this means their economies will no longer be able to grow enough to lift their people out of poverty, they will not do it. No matter how many economists flap their elbows and screech “Put a price on carbon!!”, China and the other countries of Asia will simply not limit their growth to an appreciable degree. They refused to do it at the Paris climate talks and they will continue to refuse. Carbon tariffs, carbon clubs, and other rich-country incentives will not be sufficient to persuade them.

As Biden’s economic advisors recognize, the only way China et al. will decarbonize is if doing so does not substantially hurt their economies. Thus, the whole framework that economists use for thinking about climate change — a big fat tradeoff between roasting the planet and tanking the economy — just won’t work here.

Fortunately, there is a second market failure at work here — one that can be leveraged to fight climate change without a severe tradeoff between the economy and the environment. It is one that economists, in their zeal to promote their darling carbon tax, have almost completely ignored. It is the positive externality of technology.

Ramez Naam, a technologist who has been remarkably prescient about green energy, has a great thread about how focusing on improving green technology creates less of an economic tradeoff than focusing on reducing demand for fossil fuels via a carbon tax. Here are a few tweets from that thread:

As Ramez notes, carbon taxes are good policy. They’re just limited policy. Economists have been so monomaniacally focused on how econ-y the carbon tax is that they’ve failed to consider alternatives that are more cost-effective and politically feasible. That’s why the technologists like Ramez and the activists of the Green New Deal have gotten this one right, and the economists have been left out in the cold. And it’s probably a big part of why the Biden administration is listening to the technologists and the activists instead of to the economists.

How to fix climate economics

From this litany of failures, I would suggest the following steps for climate economics to make itself more relevant:

Publish more climate economics papers.

Push back harder against shoddy methods.

Reevaluate the DICE Model.

Think more about tail risks.

Start thinking a lot more about technology.

Start thinking a lot more about the international aspect of decarbonization.

Stop focusing so much on carbon taxes.

I do believe that economists still have time to have an important, positive impact on climate policy. But the failures of the past cannot be allowed to persist into the future. It’s time for a course correction.

Update: As expected, a number of climate economists popped up on Twitter to remind me that lots of good climate econ research is, in fact, getting done. It’s often getting done by younger and/or less famous people, it tends not to be published in top econ journals (or, sometimes, in econ journals at all!), and it’s mostly fairly recent stuff (within the last decade, and especially within the last half-decade). This is absolutely true. And these people generally know what needs to be done to improve the field. But — just as with macroeconomics after 2008 — I think it will take a long time before the new crop of climate economists dig the field out of the hole of reduced credibility and prestige that it dug from the 90s through the early 2010s. Old guys who were writing papers about how climate change is good for agriculture 15 or 20 years ago are still in positions of prominence and authority. Climate change minimizers are still citing the old papers. The top econ journals are still not publishing many climate papers. Most public policy advocacy still seems quite focused on the carbon tax. Nordhaus’ Nobel (and Weitzman’s lack of Nobel) was just three years ago. There are good people working very hard on turning the ship around, but these ships tend to turn very slowly.

Update 2: Gernot Wagner, a climate economist, has a good piece in Project Syndicate on the problems with climate economics, and the way forward.

An interesting post. Canada's been very active on climate policy in the last few years, and economists have played a major role. We seem to have settled on a carbon tax as the backbone of climate policy, despite the high political cost. There's complementary measures, like phasing out coal-fired power by 2030, and some provinces have put a zero-emissions-vehicle mandate in place, but the national carbon price floor - currently C$40/t, rising to $170/t by 2030 - is the centerpiece of the plan. (It's a "price floor" because each province can either set up carbon pricing itself, in which case none of the money leaves the province, or the federal government will do it for them via a federal carbon tax backstop, with the revenue divided up and returned directly to households in the province as a dividend.)

Mark Jaccard, a veteran of the battles over BC's carbon tax, argues that flexible regulations aimed at the power and transport sectors would arouse far less political resistance, while still being reasonably cost-effective. Like you, he thinks that economists who say that a carbon tax is the optimal policy are ignoring political reality. https://www.cambridge.org/core/books/citizens-guide-to-climate-success/we-must-price-carbon-emissions/66AEBB8BE9A7F7760DC1BCE3A9C50748/core-reader

In the Canadian context, a big challenge is that Alberta and Saskatchewan are responsible for a very large share of emissions. One of the advantages of the national carbon price floor is that it lets us coordinate action across provinces, without having to sit down and work out a distribution of Canada's total carbon budget. (That would be a recipe for endless bitter wrangling, since it's zero-sum.) https://twitter.com/andrew_leach/status/1381823072181776385?s=20

I expect that the Biden and Trudeau governments will be working together on climate policy, likely on a sector-by-sector basis - power, transport, etc. Maybe some kind of carbon tariff (given tensions with China, and China's relatively new fleet of coal-burning power plants). I'm curious to see how this will play out.

Happy Birthday!!! Thanks for the consistently thought-provoking newsletter!