What Studwell got wrong

What Studwell got wrong

A few flaws in my favorite book about development

As any longtime reader of mine will know, my favorite book about economic development is Joe Studwell’s How Asia Works. If you haven’t read this book, you should definitely remedy that. In the meantime, you can start with Scott Alexander’s excellent summary.

I like How Asia Works because it tells a coherent story about how countries get rich. Basically, Studwell says it’s a three-step process:

Land reform: Forcibly buy up tenant farms from landlords and give it to the tenants; this increases farm productivity per unit of land area, gives rural people more to do, provides small farmers with some startup capital should they choose to sell their farms and move to town, and pushes landlords themselves to move to cities and use their talents to start more productive businesses.

Export discipline: Push companies to export instead of just selling domestically. Cut off support to companies that try to export and fail. This will push companies to increase productivity in order to compete in world markets, especially by learning foreign technology.

Financial control: Push banks to support exporters instead of putting their money into real estate bubbles and the like.

It’s very difficult to test whether this model really works, or whether the successful development of countries like South Korea and Taiwan was due to something else. We can look at evidence for pieces of the theory — for example, the idea that small farms tend to be more productive than medium-sized ones seems fairly well-supported in the data, and there’s also some evidence that pushing companies to export does cause them to raise their productivity.

But Studwell’s model is so complex that it’s hard to test all the pieces together. And if you need all the pieces in place — for example, if export promotion doesn’t work without the “discipline” of winding up failing firms, or if land reform fails if you don’t allow farmers to sell their land, or if export discipline itself doesn’t work without land reform — then testing the pieces individually won’t give us the answers we want.

Because it’s so hard to test, the theory serves less as a tried-and-true policy prescription and more as a launching point for ideas about how to manage a developing economy. Encouragingly, the book looks to have sparked a change in economists’ attitudes toward industrial policy — even the IMF, which Studwell castigates for having discouraged smart pro-growth policies, is now thinking carefully about the ides in Studwell’s book.

But despite its value as a source of ideas, How Asia Works shouldn’t be treated as the Bible of development. Not only are its ideas hard to verify in their totality, but Studwell does make a few mistakes in his analysis of the economies of East Asia.

South Korea vs. Taiwan

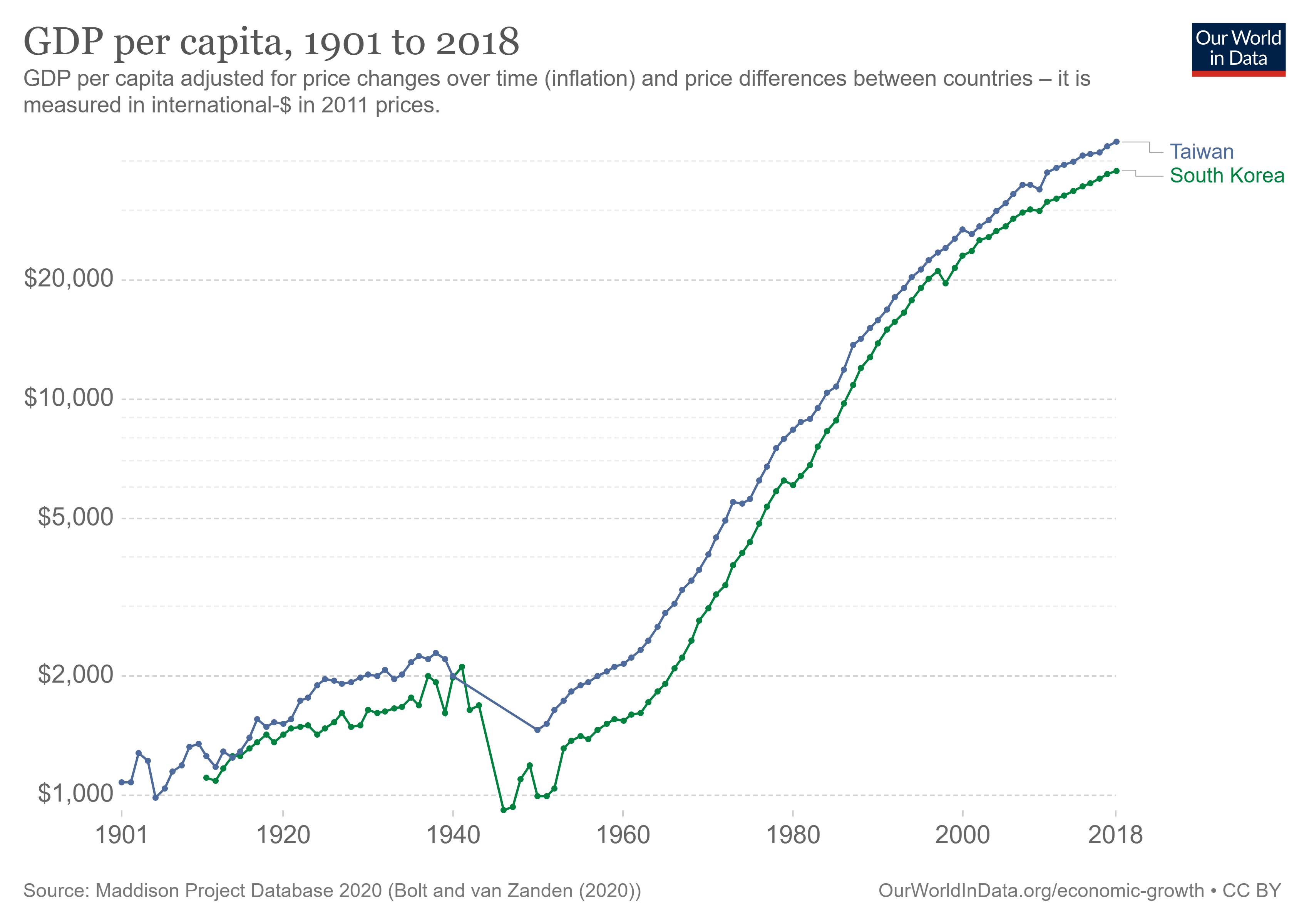

Studwell views South Korea as the development success par excellence. Though he holds up Taiwan’s land reform program (the “land to the tiller” policy) as the world’s best, he believes that Korea executed export discipline more effectively. This, he argues, is why South Korea sits ahead of Taiwan in the per capita GDP rankings.

But those rankings are calculated at market exchange rates. When you instead adjust for purchasing power parity, it turns out that Taiwan is about $6700 richer than South Korea in per capita terms, and that this disparity has existed for quite some time:

While nominal GDP (i.e., GDP measured at market exchange rates) is important for determining a country’s purchasing power on world markets, PPP is a better comparison for comparing living standards across countries. For example, suppose two countries have equal GDP per capita in dollars, but that in the second country, health care and housing are much cheaper in dollar terms than in the first country. The people in the second country are living a more affluent lifestyle, because their dollars can buy more stuff. There are various reasons why purchasing power differs between countries (the most famous being the Balassa-Samuelson effect), but the differences really do exist.

Now, there are many problems with PPP calculations. To compare the price of housing in Mozambique with housing in Switzerland, you can’t just assume that a house in the former is equal to a house in the latter — you have to adjust for the quality of the two houses, and that’s hard to do. Also, people in different countries consume different things — if Americans are kicking back in their giant houses and watching football on their big-screen TVs out in the suburbs while Japanese people are taking their excellent trains through clean, efficient cities to drink expensive liquor at trendy bars, who’s really richer than whom? And so on.

But for Taiwan and South Korea, the PPP comparison is probably pretty easy. Their development levels, urbanization patterns, and consumer tastes aren’t quite the same, but they’re probably similar enough where PPP adjustments don’t involve a ton of guesswork. And PPP shows that Taiwan is richer than South Korea — the opposite of what Studwell thinks. (For what it’s worth, their inequality levels are also very similar — both have Gini coefficients in the low to mid 30s.)

So the time and effort that Studwell puts into coming up with reasons why South Korea has done a bit better than Taiwan is probably wasted; South Korea simply has a slightly more expensive currency. (Update: Paul Krugman thinks there’s something fishy in the Taiwanese PPP numbers, but can’t quite put his finger on it. I suspect that it’s just cheap health care and housing, but it’s always worth looking into these numbers.)

Malaysia’s success

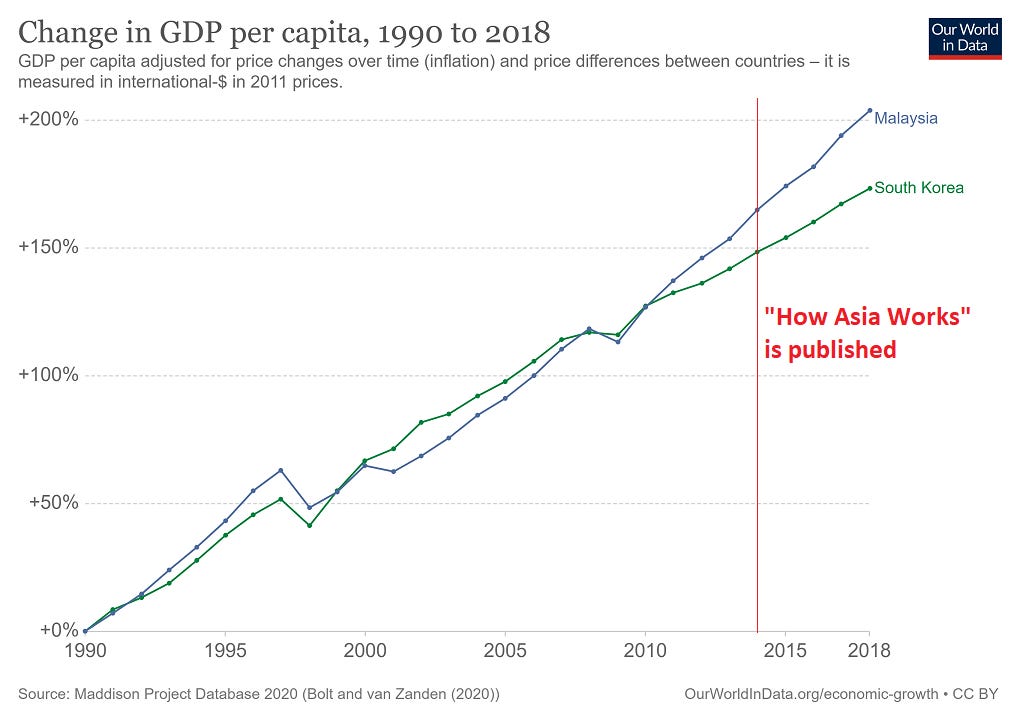

Studwell’s biggest mistake, however, is writing off Malaysia. He has two excellent, richly detailed chapters describing the history of Hyundai’s success and contrasting it to the general failure of Proton, Malaysia’s indigenous car company. Studwell generalizes Proton’s failure to represent the failure of Malaysian industrial policy writ large.

But Proton was not all she wrote when it comes to Malaysian development. The country has been far more successful in the electronics industry than the auto industry. When How Asia Works was published in 2014, Malaysia already had a bigger market share of global integrated circuit and electronic components exports than Japan, and almost as large a market share as the U.S., despite having a much smaller population than either. In some areas, it exceeds the U.S.

Now, it’s important not to overplay this success. Measuring exports doesn’t take value added into account; Malaysia only adds about 25-35% of the value in the electronics it makes. It’s a lot better at making circuits than designing them. And Malaysia has failed so far to develop internationally recognized brands — it’s still mostly a contract manufacturer for multinational companies.

Still, Malaysia’s qualified success in electronics has helped propel solid, steady growth. Malaysia has a per capita GDP (PPP) about 62% as large as South Korea's. For many years before How Asia Works was written, Malaysia grew at about the same rate as South Korea, but from a smaller base — this is somewhat of a development failure, since poorer countries ought to catch up with rich ones. But just before the book came out, South Korea slowed a bit while Malaysia kept going strong:

That means Malaysia is now catching up with South Korea, albeit slowly. That’s a development success.

Southeast vs. Northeast

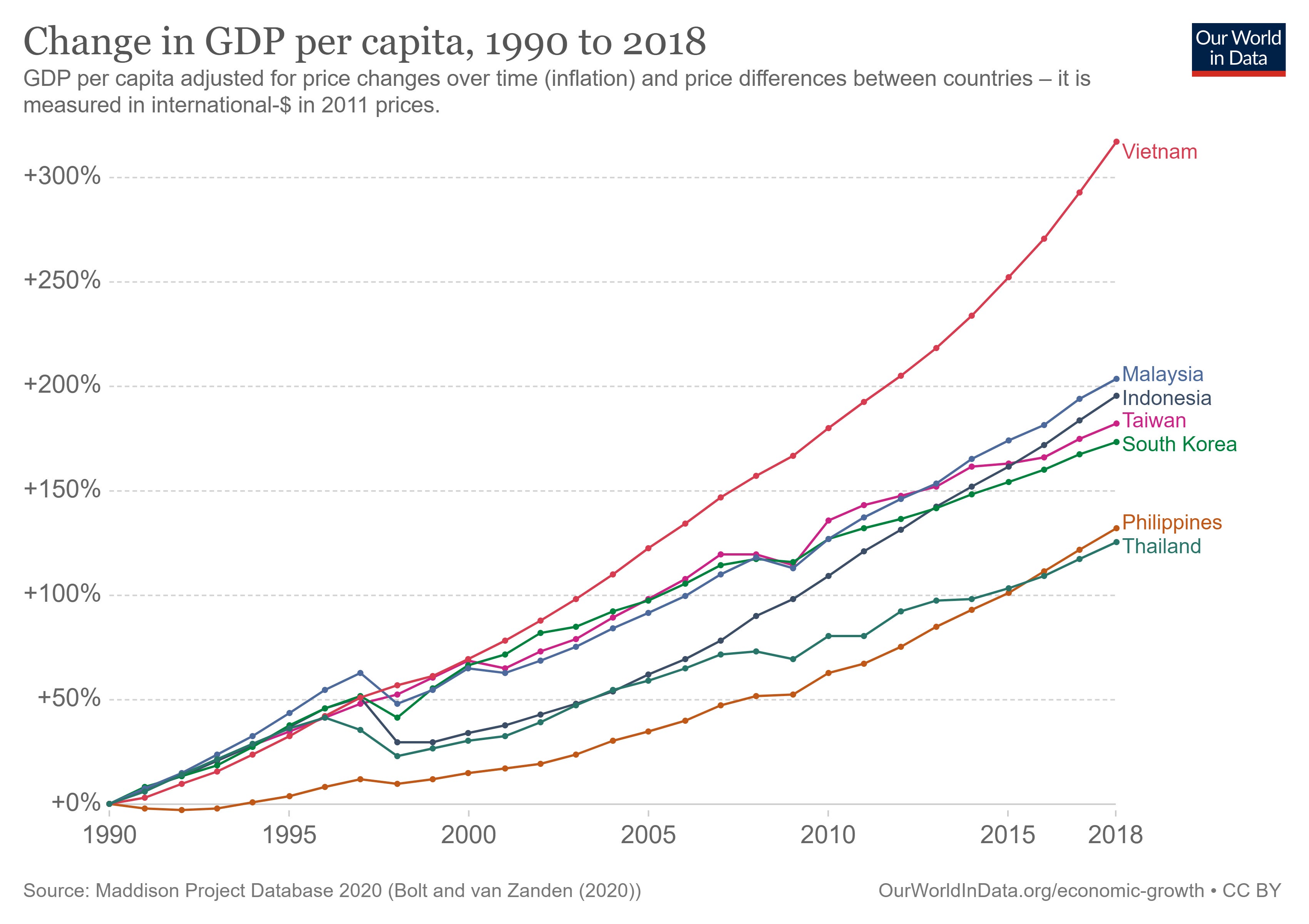

In fact, How Asia Works may have made a more general mistake by focusing only on failures when it came to Southeast Asian countries and contrasting these with successes in Northeast Asian countries. This opened the book to one big criticism — the hypothesis that Northeast Asia simply has advantages that Southeast Asia lacks, and that these advantages, not better policy, explain the differing growth outcomes.

But over the last decade, Southeast Asian countries have showed some signs of starting to catch up with their neighbors to the north:

What should we conclude if this continues for another decade or two? We might look at the particulars of Southeast Asian industrial policy, and how it changed since earlier times, and ascribe its success to those changes.

…Or, we might start to wonder if successful development policies simply determine countries’ place in a queue. My longtime readers will also know that in addition to How Asia Works, I love Krugman, Fujita, and Venables’ The Spatial Economy. And in the final section of that (highly technical) book, the authors turn what was a humble theory of urbanization into a grand theory of global development. And the upshot of that grand theory is that countries have to basically wait in line to get rich. There’s just no way for them to all hop on the rapid industrialization train all at once. Better policy can let you cut to the front of the line, but then the countries you cut in front of are out of luck.

To be sure, this is a highly stylized, pretty speculative theory, which is even harder to prove than Studwell’s. But it kinda-sorta fits the observed pattern in Asia — first Japan and Hong Kong and Singapore grew quickly, then Taiwan and South Korea, then China, now Vietnam and Indonesia. Malaysia and Thailand got a head start on China but then slowed down after the financial crisis of ‘97, while China accelerated — perhaps because China “cut in line” in front of the Southeast Asian tigers. But now, with China slowing down, perhaps Malaysia is back at the front of the line.

Anyway, this would be a depressing, fatalistic sort of world, where development is a zero-sum-game in the short term. Hopefully it’s not true — I’d much rather believe in a Studwellian world where the right smart growth policies can boost lots of countries at once. But we may never know which is right.

I love when a couple bloggers I read start discussing a book that is somewhere on my queue of to-read, but the queue is realistically growing faster than books are moving forward on it.

It sure feels like most success stories use the variables in some idiosyncratic combination - export discipline, land reform, financialisation - with the idea that implementing those variables also brings with it state legibility and accountability (not a guarantee). Which means it kind of comes down to the state, in some deep meaningful sense, deciding that it wants progress and aligning the various parts to act in concert. If there are factions fighting against it insidiously (as opposed to outright opposition, which is fine) through delays or corruption, this wouldn't work. The ur-capability seems to be to engender some level of professionalism within the state capacity to get things done.