A failed economic theory of everything

A failed economic theory of everything

For a brief moment, some economists thought they had it all figured out. They didn't.

I get kind of nostalgic and wistful when I think back to a time that it felt like macroeconomic theory actually mattered. Ten years ago, when the U.S. was trying to figure out how to pull itself out of the slump created by the Great Recession, battles over ideas like Real Business Cycle Theory and New Keynesian models were fierce, urgent, and relevant. Now, macro is way down the list of anything anyone cares about, somewhere around the same level as Nancy Reagan’s hairdo or the final episode of Seinfeld.

But macroeconomic theory can still serve as an interesting, if somewhat obscure, lesson about how science works. I was thinking about this as I perused Greg Mankiw’s latest offering in the New York Times. It’s a fairly standard boilerplate op-ed about how America can’t afford a decent welfare state (wrong!). But this piece caught my eye:

Economists disagree about why European nations are less prosperous than the United States. But a leading hypothesis, advanced by Edward Prescott, a Nobel laureate, in 2003, is that Europeans work less than Americans because they face higher taxes to finance a more generous social safety net.

In other words, most European nations use that leaky bucket more than the United States does and experience greater leakage, resulting in lower incomes. By aiming for more compassionate economies, they have created less prosperous ones. Americans should be careful to avoid that fate.

Whether Americans are actually richer than Europeans, and why this might be the case, is an interesting topic that I plan to write more about. But the research Mankiw is citing is not good evidence one way or another. Mankiw is talking about this 2003 Prescott paper, entitled “Why do Americans work so much more than Europeans?” In that paper, Prescott blames high European taxes for the difference.

The data Prescott uses to support this conclusion is startlingly sparse. He looks only at seven countries — the U.S., Canada, France, Germany, Italy, Japan, and the UK — and only at one snapshot in time, 1993-1996. You’d think that one would need more data than this to support broad, sweeping conclusions about how much taxes discourage work. But for Prescott, this limitation is a feature rather than a bug.

Because Prescott’s main tool of analysis isn’t empirical; he isn’t running a regression of work hours on taxes, or anything like that. Instead, his conclusions come from a theoretical model.

Prescott’s model is a very basic version of Real Business Cycle Theory, which he developed in the 80s and won a Nobel Prize for in 2004. RBC Theory was developed to explain why economies have booms and busts. In brief, it says that booms and busts are both caused by random fluctuations in the rate of technological progress — when scientists and engineers develop less useful stuff, there’s a recession. Unemployment, in this model, is simply workers deciding to work less because their wages are growing more slowly due to slower technological progress.

If that sounds like a ridiculously unrealistic description of how the economy works, well, that’s because it is. Economists at the time who weren’t caught up in the rush of excitement over having a new theoretical tool to play with instantly recognized that the model required highly unrealistic parameter values in order to match even the most basic facts about recessions. Later, a flood of empirical research showed how poorly RBC models fit the data, while a flood of theoretical papers showed how just adding a few tiny realistic wrinkles to the model could reverse its implications utterly.

Faced with the basic model’s empirical failures and theoretical non-robustness, proponents of the RBC idea made various modified versions, most of which also didn’t do incredibly well, but which spawned a major research effort at the University of Minnesota and a few other schools. Meanwhile, most macroeconomists moved on to other theories like New Keynesian theory — which were based on the mathematical framework that RBC pioneered, but relied on very different economic mechanisms — to explain booms and busts. The fact that Prescott won the Nobel for RBC in 2004, even after its many failures, is a vivid demonstration of the fact that the Econ Nobel is a prize given for the development of new methods, rather than the achievement of solid scientific results.

But Prescott’s paper on Europe shows the breathtaking scope of the RBC theorists’ ambitions for their theory. What Prescott does in that paper is to plug his favorite parameter values into a basic RBC model, use the results to predict how much work hours will depend on taxes, and then compare those predictions with a few other countries in the mid-90s. In other words, he takes a simple model that was developed to explain booms and busts, and uses it to explain long-term differences in work hours.

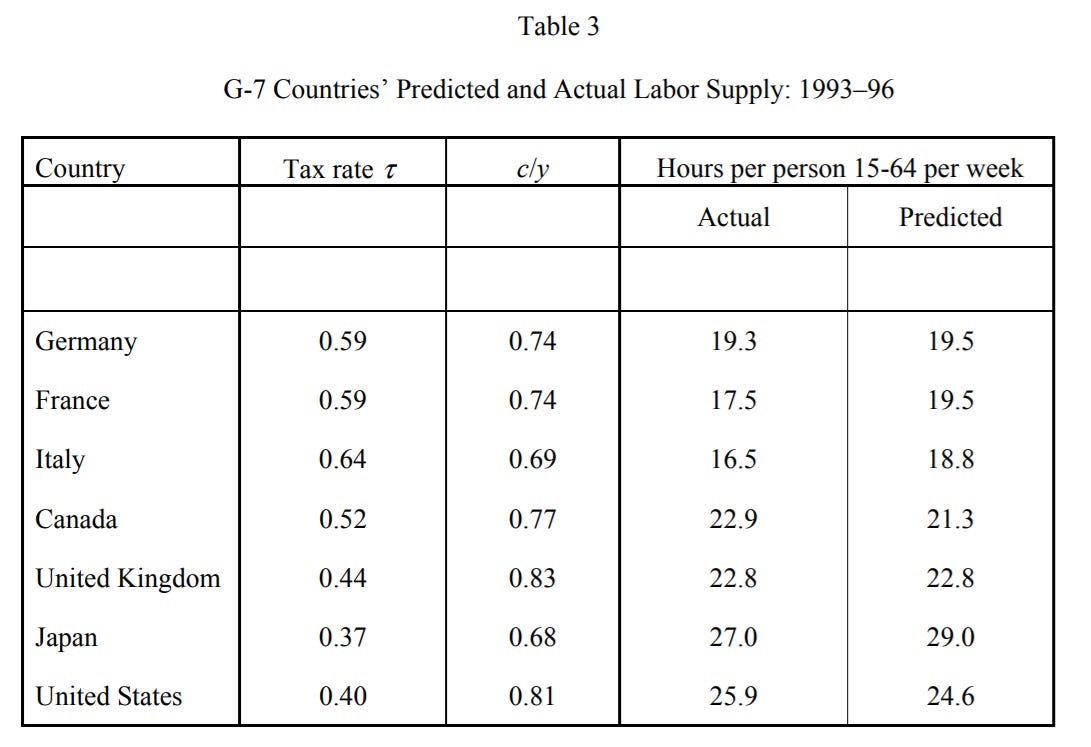

Here are his results:

Prescott looks at this table and basically says “Hey, looks pretty good!” There’s no attempt to statistically quantify how good the results are — no confidence interval, nothing that would tell us whether an average prediction error of 1.14 hours per week is significant in a data set where the standard deviation is 4 hours per week. Prescott just says it’s a “surprisingly small” difference.

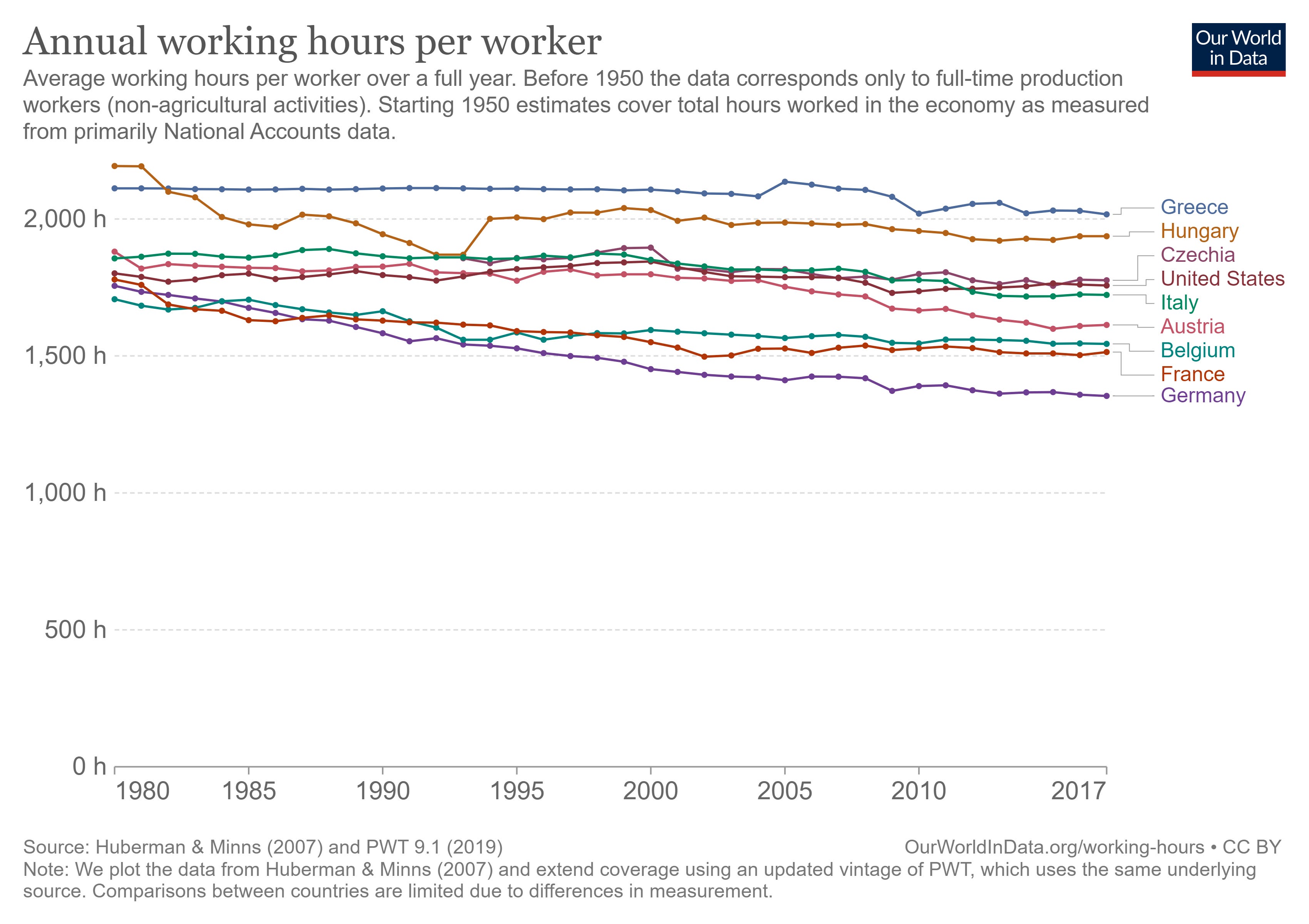

Nor does Prescott attempt to extend the analysis to a wider range of countries. If he did, he might have noticed the existence of countries like Hungary, Greece, and Czechia, which work more than the U.S. despite having some of the highest tax burdens on labor:

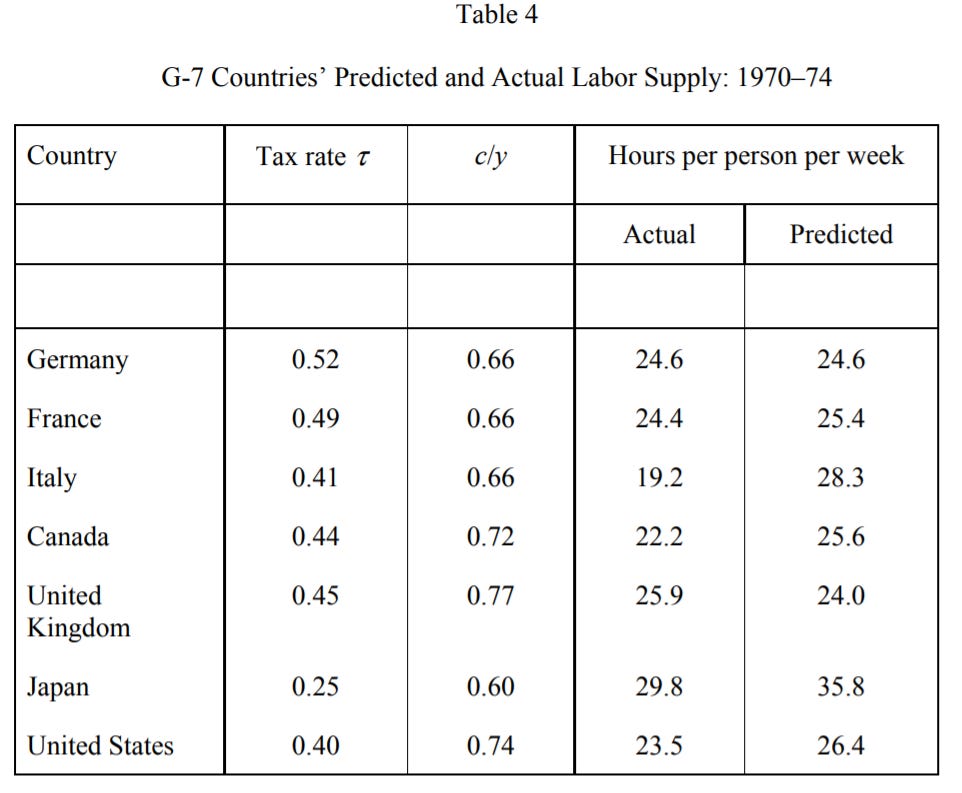

Nor does Prescott do much analysis of movements in labor hours over time — a startling omission, considering that RBC theory was developed to explain fluctuations in employment. Prescott does apply his analysis to another snapshot, in the early 1970s. And though the model seems to work for several of the countries, it has huge misses for Italy and Japan:

Prescott explains away these misses by attributing them to peculiar labor institutions in 1970s Italy and Japan. He does not consider whether labor institutions are substantively different among the other countries in the sample, or whether labor institutions were different in the 90s. When his model yields good predictions, Prescott concludes that all the stuff outside the model is being “averaged out”; when it yields bad predictions, he invokes additional factors in an ad-hoc fashion.

Most people would say that this is not a very good way to do science, I think. Most people would agree that a model should be tested against as much data as possible, to find out how useful of a model it really is, and conditions under which it is and isn’t useful, rather than comparing it to only just enough data to generate a few good-looking point estimates and calling it a day.

And — surprise! — Prescott’s method of analysis led to results that didn’t hold up when economists took careful stock of the microeconomic evidence. Micro studies show that taxes don’t discourage work nearly as much as Prescott concludes. In fact, the only way for Prescott’s model to explain the differences in working hours between countries would be for changes in tax rates to induce a bunch of people to quit working entirely — something that we just don’t see happening. The differences in work hours between the U.S. and other rich countries are probably due mostly to things other than tax rates.

Of course, people who want to argue that high taxes will discourage work still cite Prescott’s paper.

But like I said, what’s really interesting to me is how much Prescott’s paper tries to expand the explanatory scope of his simple theory. Going from a theory of business cycles to a theory of long-term work hours and taxation, without any change in the model, is a startling degree of mission creep. It suggests that what Prescott was really hoping to do with the RBC model wasn’t just to explain booms and busts — it was to create an economic theory of everything, a simple theoretical framework that could be applied to practically any phenomenon with minimal modification.

That was obviously never going to happen. Economic models are used for very specific applications precisely because their explanatory power is generally weak; trying to take them beyond the context for which they were developed typically results in very silly predictions very rapidly. And RBC wasn’t even good at explaining the one thing it was designed to explain! So turning it into a theory of everything was always an unrealistic project.

I would like to say that this offers a cautionary tale, both for people in other social-science fields, and for the economic theorists of the future. But Prescott’s Nobel shows that when theories aren’t good at matching data, they tend to get rewarded for methodological innovation instead. It’s even possible that by trying to expand RBC’s explanatory power beyond its original mission, Prescott made his theory seem even more novel and influential than it already was — after all, though the practice of plugging anything and everything into an RBC model never caught on, he won the Nobel the year after his paper on Europe came out. We humans tend to like our Great Big Theories of Everything, even when they aren’t, you know, right.

Wow that is just a shockingly bad take from Mankiw. I remember even in the econ 101 textbook I got, in the chapter about basic concepts of supply and demand, they discussed the possibility that the curves might sometimes be wonky, and they very specifically used the wage / leisure trade-off to illustrate this -- sometimes when people get richer (higher wages) they will choose to "spend" some of those gains by way of working less, and it's entirely possible that the equilibrium might have lower headline income. (But if working fewer days lowers commute costs, or provides intangible benefits, like unpriced-but-valuable time with family, this can still result in a net improvement in the earner's welfare.)

Many popular economists act more like mass psychology gurus than empirical scientists.